2.2: The Function e^x

- Page ID

- 9955

Many of you know the number e as the base of the natural logarithm, which has the value 2.718281828459045. . . . What you may not know is that this number is actually defined as the limit of a sequence of approximating numbers. That is,

\[e=\lim_{n→∞}f_n \nonumber \]

\[f_n=(1+\frac 1 n)^n\;,\;n=1,2,... \nonumber \]

This means, simply, that the sequence of numbers \((1+1)^1,(1+\frac 1 2)^2,(1+\frac 1 3)^3, . . . \), gets arbitrarily close to 2.718281828459045. . . . But why should such a sequence of numbers be so important? In the next several paragraphs we answer this question.

(MATLAB) Write a MATLAB program to evaluate the expression \(f_n=(1+\frac 1 n)^n\) for \(n=1,2,4,8,16,32,64\) to show that \(f_n≈e\) for large \(n\).

Derivatives and the Number e

The number \(f_n=(1+\frac 1 n)^n\) arises in the study of derivatives in the following way. Consider the function

\[f(x)=a^x\;,\;a>1 \nonumber \]

and ask yourself when the derivative of \(f(x)\) equals \(f(x)\). The function \(f(x)\) is plotted in the Figure for \(a>1\). The slope of the function at point \(x\) is

\[df(x)dx=\lim_{Δx→0}{\frac {a^{x+Δx}−a^x} {Δx}} = α^x \lim_{Δx→0} {\frac {α^{Δx}−1} {Δx}} \nonumber \]

If there is a special value for \(a\) such that

\[lim_{Δx→0} \frac {a^{Δx}−1} {Δx}=1 \nonumber \]

then \(\frac d {dx} f(x)\) would equal \(f(x)\). We call this value of a the special (or exceptional) number \(e\) and write

\[f(x)=e^x \nonumber \]

\[\frac d {dx}f(x)=e^x \nonumber \]

The number \(e\) would then be \(e=f(1)\). Let's write our condition that \(\frac {a^{Δx}−1} {Δx}\) converges to 1 as

\[e^{Δx}−1≅Δx\;,\;Δx\;\mathrm{small} \nonumber \]

or as

\[e≅(1+Δx)^{1/Δx} \nonumber \]

Our definition of \(e=\lim_{n→∞}(1+1n)^{1/n}\) amounts to defining \(Δx=\frac 1 n\) and allowing \(n→∞\) in order to make \(Δx→0\). With this definition for \(e\), it is clear that the function \(e^x\) is defined to be \((e)^x\):

\[e^x=\lim_{Δx→0}(1+Δx)^{x/Δx} \nonumber \]

By letting \(Δx=\frac x n\) we can write this definition in the more familiar form

\[e^x=\lim_{n→∞}(1+\frac x n)^n \nonumber \]

This is our fundamental definition for the function \(e^x\). When evaluated at \(x=1\), it produces the definition of \(e\) given in Equation.

The derivative of \(e^x\) is, of course,

\[\frac d {dx} e^x = \lim_{n→∞}n(1+\frac x n)^{n−1}\frac 1 n = e^x \nonumber \]

This means that Taylor's theorem1 may be used to find another characterization for \(e^x\):

\[e^x=∑^∞_{n=0}[\frac {d^n} {dx^n} e^x]_{x=0} \frac {x^n} {n!} = ∑^∞_{n=0}\frac {x^n} {n!} \nonumber \]

When this series expansion for \(e^x\) is evaluated at x=1, it produces the following series for e:

\[e=∑_{n=0}^∞\frac 1 {n!} \nonumber \]

In this formula, \(n!\) is the product \(n(n−1)(n−2)⋯(2)1\). Read \(n!\) as "n factorial.”

(MATLAB) Write a MATLAB program to evaluate the sum

\[S_N=∑_{n=0}^N\frac 1 {n!} \nonumber \]

for \(N=1,2,4,8,16,32,64\) to show that \(S_N≅e\) for large \(N\). Compare \(S_{64}\) with \(f_{64}\) from Exercise 1. Which approximation do you prefer?

Compound Interest and the Function ex

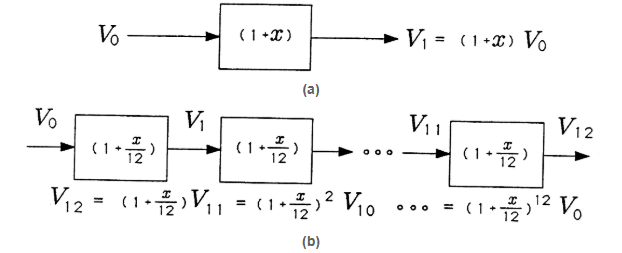

There is an example from your everyday life that shows even more dramatically how the function \(e^x\) arises. Suppose you invest \(V_0\) dollars in a savings account that offers 100x% annual interest. (When x=0.01, this is 1%; when x=0.10, this is 10% interest.) If interest is compounded only once per year, you have the simple interest formula for \(V_1\), the value of your savings account after 1 compound (in this case, 1 year):

\(V_1=(1+x)V_0\). This result is illustrated in the block diagram of the Figure. In this diagram, your input fortune \(V_0\) is processed by the “interest block” to produce your output fortune \(V_1\). If interest is compounded monthly, then the annual interest is divided into 12 equal parts and applied 12 times. The compounding formula for \(V_{12}\), the value of your savings after 12 compounds (also 1 year) is

\[V_{12}=(1+\frac x {12})^{12}V_0 \nonumber \]

This result is illustrated in Figure. Can you read the block diagram? The general formula for the value of an account that is compounded n times per year is

\[V_n=(1+\frac x n)^nV^0. \nonumber \]

\(V_n\) is the value of your account after n compounds in a year, when the annual interest rate is 100x%.

Verify in the Equation that a recursion is at work that terminates at \(V_n\). That is, show that \(V_i+1=(1+\frac x n)V_1\) for \(i=0,1,...,n−1\) produces the result \(V_n=(1+\frac x n)^nV_0\).

Bankers have discovered the (apparent) appeal of infinite, or continuous, compounding:

\[V_∞=\lim_{n→∞}(1+\frac x n)^nV_0 \nonumber \]

We know that this is just

\[V_∞=e^xV_0 \nonumber \]

So, when deciding between 100x2% interest compounded daily and 100x2% interest compounded continuously, we need only compare

\[(1+\frac {x_1} {365})^{365}\;\;versus\;\;e^{x_2} \nonumber \]

We suggest that daily compounding is about as good as continuous compounding. What do you think? How about monthly compounding?

(MATLAB) Write a MATLAB program to compute and plot simple interest, monthly interest, daily interest, and continuous interest versus interest rate 100x. Use the curves to develop a strategy for saving money.

Footnotes

Taylor's theorem says that a function may be completely characterized by all of its derivatives (provided they all exist)